Are you presently eager to own property of your? If that is your ideal, youre most likely saving right up, money by the hard-received buck, until you get that miracle count: 20% of your dream house’s full well worth to your down payment. That is what every pros state, correct?

On the mediocre American household, 20% quantity so you’re able to a pretty big number. Throw in settlement costs along with lots of money so you’re able to improve and you can age commit until you achieve your purpose.

It’s great that you will be getting money aside toward what’s going to almost certainly end up being the biggest purchase of your life, but there’s one to grand mistake on your own data: It’s not necessary to generate a great 20% down-payment.

Sure, you realize best. New 20% misconception is actually a sad kept in the point in time adopting the houses crisis when regarding necessity, usage of credit fasten. Thank goodness, minutes features altered, and since FHA money were launched over 80 years back, mortgages haven’t expected good installment private loans Cincinnati 20% down payment.

While it’s correct that a top down-payment mode you have an inferior month-to-month mortgage repayment, there are many reason why it isn’t really a knowledgeable road to homeownership.

Let us explore loan selection that do not wanted 20% down or take a further look at the pros and cons of creating an inferior down payment.

Financing alternatives

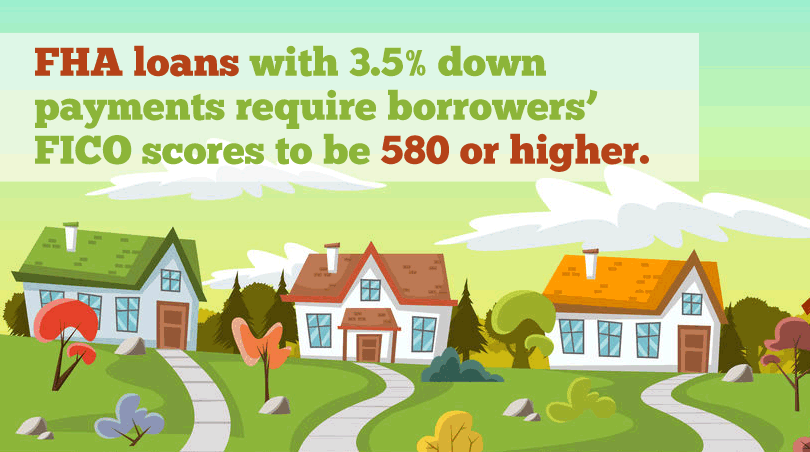

1.) FHA home loan: That it mortgage is aimed at helping first-go out home buyers and needs only step three.5% off. If that matter remains too much, brand new downpayment can be sourced away from an economic provide or through a downpayment Guidance system.

2.) Va home loan: Va mortgage loans would be the extremely forgiving, but they are purely to own newest and you may former army users. Needed zero down, don’t need mortgage insurance coverage and accommodate all of the closing costs in the future from a seller concession or gift fund.

step 3.) USDA home loan: These types of financing, backed by the usa Service off Farming, additionally require no off, however, qualifications try venue-built. Being qualified house doesn’t have to be found on farmlands, but they need to be during the sparsely populated portion. USDA financing can be found in every fifty says and are usually provided from the extremely lenders.

1.) 3% off home loan: Many lenders usually today offer mortgage loans which have borrowers placing only a small amount due to the fact step three% off. Some loan providers, particularly Freddie Mac, even give less mortgage insurance on these money, without income constraints no earliest-day client requirement.

dos.) 5% off home loan: A lot of lenders enables you to put down merely 5% out of a great home’s worthy of. Although not, extremely believe your house become buyer’s number one household and you may the buyer enjoys an effective FICO score off 680 or even more.

3.) 10% off mortgage: Extremely loan providers makes it possible to take out a conventional mortgage which have 10% down, even with a less-than-most readily useful credit history.

Bear in mind that all these finance demands money qualifications. Likewise, getting lower than 20% off results in buying PMI, otherwise individual home loan insurance. However, for those who view your residence once the an asset, expenses your PMI feels as though paying to your a good investment. In reality, based on TheMortgageReports, certain property owners enjoys invested $8,100 during the PMI over the course of ten years, in addition to their residence’s really worth has increased from the $43,100. Which is a large profits on return!

Whenever you are considering wishing and you can protecting until you has actually 20% to put upon a property, think of this: A beneficial RealtyTrac investigation learned that, normally, it can simply take a home visitors nearly 13 years to store for a 20% advance payment. In most that time, you may be strengthening your collateral and you can home values could possibly get increase. Costs more than likely usually too.

Other positive points to getting down lower than 20% include the after the:

- Rescue bucks: You have more cash open to invest and save.

- Repay loans: Of numerous loan providers highly recommend playing with offered dollars to spend off bank card loans before purchasing a home. Credit debt typically has increased interest rate than simply financial debt plus it wouldn’t internet you a tax deduction.

- Change your credit history: Once you have repaid obligations, expect to see your get surge. You are able to residential property a far greater mortgage rate that way, particularly when the rating passes 730.

- Remodel: Few residential property have been in best standing due to the fact offered. You will probably want to make certain alter into the new home before you move around in. That have some money readily available makes it possible to do this.

- Generate an urgent situation financing: Since the a resident, having a properly-stocked crisis money is essential. From this point on, you will end up one investing to fix any plumbing system affairs or leaky roofs.

Cons regarding an inferior down-payment

- Home loan insurance: An excellent PMI commission was an extra monthly expense loaded on top of the financial and you may possessions income tax. As mentioned more than, even in the event, PMI is a good investment.

- Possibly highest home loan rates: When you’re taking right out a traditional financing and you will making an inferior downpayment, could features a high home loan speed. Yet not, if you find yourself taking out a federal government-recognized mortgage, you may be protected a lowered financial rates even with a faster-than-strong advance payment.

- Less equity: You have less guarantee of your property having a smaller off commission. However, unless you’re browsing offer in the next while, this ought not to have any tangible affect the homeownership.

Without a doubt, this doesn’t mean you can buy a property no matter how far otherwise exactly how nothing you have got on the family savings. Prior to that it decision, be sure you really can manage to individual a house. Ideally, the overall month-to-month housing will set you back should total less than 28% of one’s month-to-month revenues.

Ready to get your dream house? We had prefer to assist you! Call us from the Joined Colorado Borrowing from the bank Union today to know about our big financial apps and you may costs. We are going to walk you through as high as the fresh closure!

Your Change: Maybe you’ve ordered property and place below 20% off? Show your expertise in all of us regarding comments!

Recent Comments